See all results for ''

We love acronyms in finance and our industry has a bizarre way of regularly concocting harmless sounding WMD’s (Weapons of Mass Destruction). I am sure you have read in the news recently about the music band ‘Eagles’ inspired ‘Hotel California type’ gigantic NTREIT (Non-Traded Real Estate Invest Trust) which recently imposed gates on client redemptions. Prior to the US housing collapse in 2008, there were NDLC (No Docs/Low Docs) mortgages bundled into MBS’s (Mortgage-Backed Securities) and CMO’s (Collateralised Mortgage Obligations) which devastated the financial system.

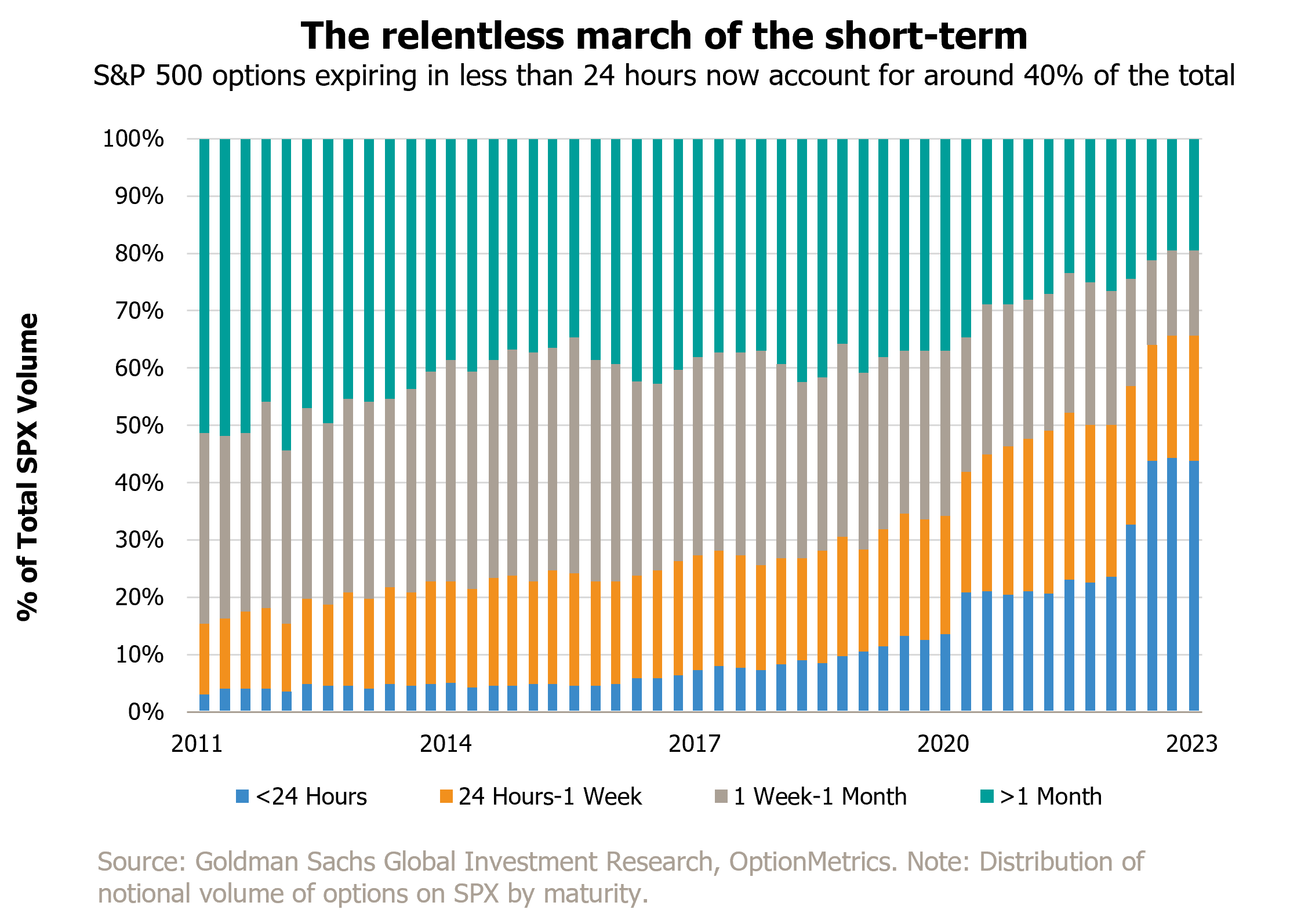

Long Term Capital Management (LTCM) infamously blew up just after the Asian financial crisis and Russia’s sovereign default in 1998. Though the name conveyed a conviction-led firm meticulously following their investment models and processes leading to lengthy holding periods, in reality, LTCM owned securities for couple of days, and at best a week. Two decades later, that holding period seems a lifetime when we look at Zero Days to Expiration (0DTE) options.

0ZTE options allow investors to buy and sell contracts that have a shelf life of less than 24 hours. By all accounts, according to Lu Wang at Bloomberg, “this is a manifestation of the new breed of ‘gamblers’ betting on daily moves and computer driven firms known to measure the life cycle of trades in thousandths of a second.” Or are they used mainly by KIPPERS (Kids in Parents’ Pockets Eroding Retirement Savings) pitting themselves against GOFS (Grey Old Patient Folks) like me?

Jack Boggle, the legendary founder of Vanguard, once put it well ‘time is your friend, impulse your enemy’. I’d rather never use an acronym for that. Fortunately, I have patience, a luxury in today’s market environment. Take AKR Corporation in Indonesia as an example. One of our largest positions in the fund today, encountered operational challenges in 2018 while simultaneously investing in their industrial estate and deep-water port joint ventures. In two years, 2018 and 2019, they had a negative free cash flow (or cash outflows) of approximately US$125m. Markets got skittish, sold down the stock. I kept my resolve, and that patience has paid off well for our clients. In three years (2020 to 2022), the company generated approximately US$485m of cash flows. In my view, this is just the start of what could be a long-term sustained improvement in cash flows as they are squarely benefiting from the transformation in Indonesia which I wrote about recently (CLICK here).

Source for all data JOHCM/Bloomberg (unless otherwise stated)

Disclaimer

For professional investors only. This is a marketing communication. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. Portfolio holdings are subject to change at any time and are not recommendations to buy or sell any security.

Indonesia is growing its economy, raising its skill levels and increasing value-added exports, using the old-fashioned method: protectionism

For a better experience, we recommend viewing this website in landscape orientation.