See all results for ''

Stereotype - a widely held but fixed and oversimplified image or idea of a particular type of person or thing.

My memories of Indonesia were burnished in 1998 when I lost my job at my then employer Peregrine Securities (a Hong Kong listed Asian investment bank). The Economist magazine declared Peregrine’s bankruptcy as ‘the first recorded instance in history where the creditor had gone bankrupt, but the debtor had survived’. The notorious debtor was Steady Safe (!) an Indonesian taxi company with some links to the then Indonesian President’s daughter. The Rupiah devalued from around 2,500/$ to almost 16,000/$. In that year, the Asian Debt Crisis, as it became known, created significant upheaval across the country.

In 2013, a comment from then-chair of the Federal Reserve, Mr. Ben Bernanke, on ‘tapering’ their asset purchase programme, led to a sequence of events resulting in a sell-side firm coining the term ‘Fragile Five’ in the emerging market space. Indonesia was one of those five countries. A current account and a budget deficit revealed vulnerabilities; the Rupiah depreciated from 9700/$ to 14,700/$. The effect on the economy was large but nowhere near the previous crisis.

Leadership makes a difference. Joko Widodo (Jokowi) was first elected President of Indonesia in 2014 and for his second and final 5-year term in 2019. Amongst his first consequential policy decisions was to double down on the partial ban of export of raw nickel ore till December 2019, and a full ban from January 2020. The objective - to build sovereignty in natural resources, add value to domestic products, increase foreign exchange revenues and create an even economic growth model. In other words, protectionism. Justified in my view and it has been spectacularly successful.

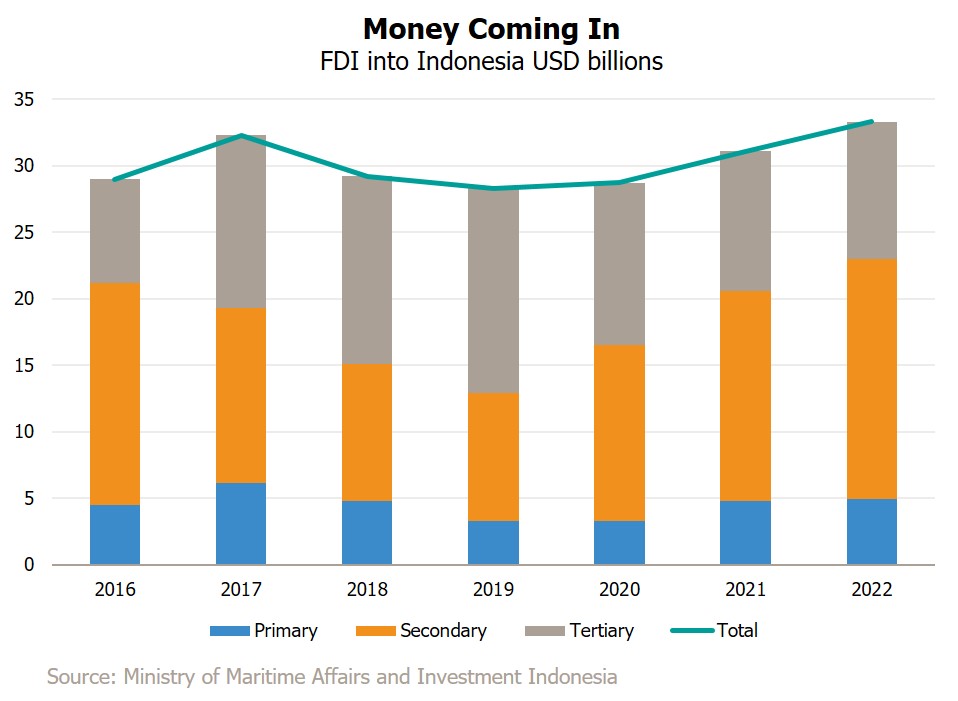

Indonesia is the world's top producer of nickel. An essential component of stainless steel, the ban spurred an influx of Chinese investment into the nickel processing industry, with dozens of smelters now operating mostly on Sulawesi and Halmahera islands. Foreign direct investment (FDI) rose while Indonesia became a large stainless-steel exporter. In 2014, nickel related exports were approximately US$1.5b. In 2023, they are estimated to reach US$30 billion. The most remarkable statistic I observed was that Indonesia might run a current account surplus with China in the next few years.

.jpg)

Their bigger plan is to try capture the electric vehicle battery supply chain and persuade firms to manufacture EV batteries at scale in Indonesia. Except lithium, the country has adequate deposits of most other minerals needed to make EV batteries. By progressively banning other mineral exports in unprocessed form (tin, bauxite, copper), they are progressively pushing companies to set up smelters or processing plants in the country and encouraging EV battery makers to set up shop in Indonesia. Incidentally, AKR Corporation (one of our holdings in the portfolio) benefits from increased imports of chemicals which smelters use copious amounts of. Moreover, at their 60% owned industrial estate JIIPE (Pelindo - a Surabaya government entity owns 40%) Freeport-McMoRan is investing US$4b in a copper smelter to be completed by early 2024.

The longer-term implications are transformational for Indonesia. No doubt these exports currently are still of value-added or processed commodities. There will be cyclical downturns and Indonesia should diversify to other sectors as well to rebalance their dependence on commodities. Yet, it is a remarkable turnaround from a raw commodity exporter to exports of processed or value-added materials. It is no mean feat to attract significant FDI into the country. If this trend continues, the previously simplified notion of Indonesia being the sick man of Asia must be challenged. Taken further out, if the country does start to generate large surpluses, there could be a potential of long-term sticky capital cushioning the currency from external shocks. The ultimate prize could be a secular decline in interest rates. That could potentially lead to higher valuation multiples for Indonesian equities as rates decline and the volatility of its currency fades. Clearly unlikely in the short run but worth keeping in mind over the long term.

Disclaimer

For professional investors only. This is a marketing communication. Information on the rights of investors can be found here. The registrations of the funds described in this document may be terminated by JOHCM at its discretion from time to time. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation.

In China, we’re investing in companies that have low valuations and rising cashflows. They aren’t the usual suspects

Until recently, the consensus was that China would decouple economically from the developed world. Now we know the separation is not economic but ideological

Higher US interest rates could present significant upside for Asian equities

For a better experience, we recommend viewing this website in landscape orientation.