See all results for ''

Talking about dividend yield in recent years has often felt futile. Companies that paid good dividends were seen as being somehow limping along in the past, as though they couldn’t think of anything better to do with their earnings than distribute them to their owners.

The high-water mark of this attitude was expressed in a well-read article published in the Financial Times in December 2021. The predominance of dividend-paying stocks in the UK was seen as a weakness. The UK equity market was described as the financial equivalent of Jurassic Park – a landscape of dinosaurs that had outlived their time. Investors seeking income from equities were told they were hardly more than parasites, sucking out cashflow rather than giving management the scope to reinvest earnings in … growth.

The Jurassic Park FT article marked the nadir of the UK equity market’s relative performance – so far this year the UK has been one of the few markets to broadly hold its ground, compared with large falls elsewhere e.g. c. 28% for the tech-heavy Nasdaq .

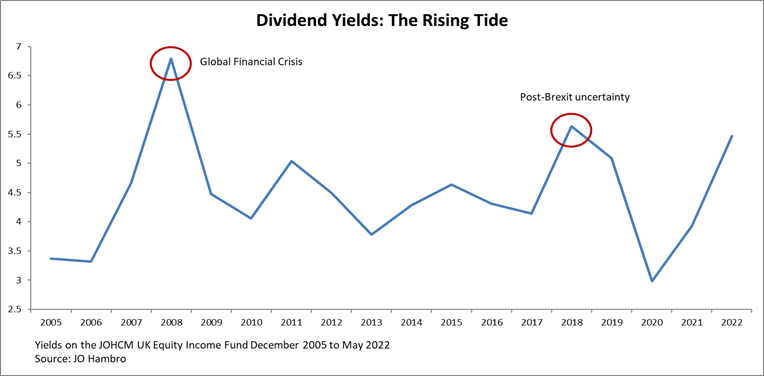

The dividend yield of the Fund for 2022 is currently forecast to be 5.5%. We believe the dividend per unit will end the year higher than pre Covid. The graph below shows the Fund dividend across the 18 years of the Fund’s life – it has only been higher during the financial crisis and as Brexit negotiation reached the point of maximum pessimism under the Theresa May government.

Compared to both of those points in time, the yield on the Fund feels very robust – balance sheets are materially better, dividend cover ratios more prudent and as we have noted before around half the Fund is currently buying back shares reflective of these circumstances.

Dividends used to be considered the vanguard of annual returns. The table below shows the split in total returns between dividends and capital appreciation over three time periods. Two points stand out immediately. One is that over the long-term – in this case over nearly 50 years – three-quarters of returns derive from dividends – this was the norm and is likely to be the norm again. The other is that this has changed over more recent timeframes, to just under half in the past 20 years and to a mere 16% in the two years to the end of 2021.

| Returns | % Accrual | ||||

|---|---|---|---|---|---|

| Global market | Total | Price | Dividends | Price | Dividend |

| Since Jan 1973 | 8971.8% | 2276.7% | 6695.1% | 25.4% | 74.6% |

| Last 20 years | 352.3% | 177.6% | 174.7% | 50.4% | 49.6% |

| Jan 20 to Dec 21 | 33.9% | 28.4% | 5.5% | 83.8% | 16.2% |

Source: Credit Suisse.

The decline in the importance of dividends over the last two decades is due to the suppression of interest rates since the Global Financial Crisis (GFC). Cheap, practically free, debt capital has encouraged investors to pursue long-duration stocks.

The reversal of this trend has come suddenly, and to a large extent unexpectedly, but it has shattered consensus positioning around growth stock’s Investors are having to re-think a generation of perceived wisdom. The suppression of interest rates driven by central bank activity, in particular, quantitative easing has led to a radical misallocation of capital. Our previous paper (see here) discussed why these growth stocks – which had reached the highest valuations they had ever got to – have fallen so much as real interest rates have risen.

This regime-shift, in our view, has only just started.

In these conditions, far from being a paleontological zoo, the UK equity market with a high starting dividend yield, strong companies, a heavy weighting towards real assets (eg mining, oil, property etc) starts looking very much in tune with current trends – more normal interest rate structures – and its outperformance year-to-date makes perfect sense.

A cash yield also provides protection against inflation – it is feasible that the average rate of inflation over 2022 and 2023 will be c. 5-6% as inflation peaks this year and falls as energy price increases are lapped. The dividend yield on the Fund – at 5.5% - noted above – offsets this - protecting value in real terms.

We showed the earlier paper (see here) that valuations within the Fund are close to all-time lows on an absolute basis. On a relative basis, due to a rush to safety, we are also back to the widest gap in valuation terms between the type of stock the Fund owns and defensives that now dominate the FTSE indices. We believe that there is material upside in the Fund and significant valuation risk lurking under the surface in certain large index components. This paper shows that whilst waiting for this upside to feed through the yield both provides protection against inflation and as it has done, over the longer term, the majority of total return. The ongoing regime change should lead to a renaissance of both the UK equity market and the UK Equity Income Sector.

James Lowen and Clive Beagles are senior fund managers on the JOHCM UK Equity Income Fund. For more information on the Fund, click below:

| Learn more about the JOHCM UK Equity Income Fund |

Disclaimer

For professional investors only. This is a marketing communication. Information on the rights of investors can be found here. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation.

In an environment of higher inflation, investors should increasingly favour dividend-paying stocks

Rising yields are presenting interesting opportunities to income investors

For a better experience, we recommend viewing this website in landscape orientation.