See all results for ''

Data is the new Oil. China has nationalised it, Europe is trying to regulate it (GDPR) while the US is divided on philosophical grounds. India, on the other hand, is doing something radical about it - by utilising Account Aggregators (AAs).

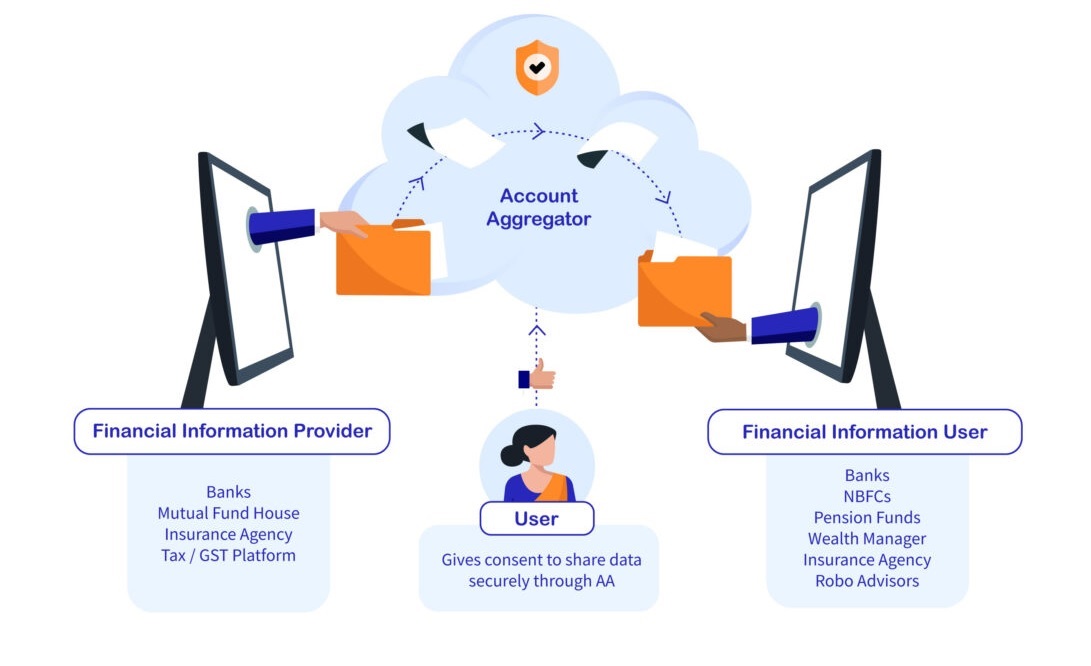

What is an Account Aggregator?

AA’s are intermediaries - licensed non-banking financial companies (NBFCs) – which collect and consolidate the data you provide to banks/lenders, wealth/insurance service providers, tax authorities or telecom operators (aka Financial Information Providers - FIPs) and share this data, with your consent, with Financial Information Users (FIUs). These include any institution that is registered and supervised by any of the financial sector regulators (across banking, lending, financial planning and investments, insurance and pension).

Whilst traditional credit bureaus already collect customer liability data, AAs will have access to customer assets and transaction data, which should improve data analytics. The objective is to increase financial services penetration and approval rates for loan applications while reducing transactional friction. Over time, more data (through things like GST and income tax) will flow through as well.

Source: sahamati.org.in

So what is the impact on incumbents and fintechs?

AA's represent both a challenge and an opportunity for incumbent banks and NBFCs. Sure, they lose client-exclusivity and may see higher churn rates, but the opportunity for them to gain from the widening overall market, especially SME and retail could be lucrative.

In my view, this building block will mean a wider, and better choice for consumers and give them more control over their data. Incumbents might lose their ‘moats’ of proprietary data and hence could, over time, de-rate as businesses. Fintech platforms involved in loans and marketplaces, robo-advisory companies and neo-banks may all get a boost. With AAs, competition gets a leg-up and innovative business models, unimaginable today, will spring up. We could see increased partnerships between banks, NBFCs and fintech platforms. Watch this space.

Disclaimer

Past performance is no guarantee of future performance. This is a marketing communication. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. The Fund’s investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. Information on the rights of investors can be found here.

What next for China? Samir discusses the regulatory clampdown including two other sectors not yet hit - housing and healthcare.

Should we even bother investing in China?

Quarantine musings from Samir Mehta, manager of the JOHCM Asia ex Japan Fund.

For a better experience, we recommend viewing this website in landscape orientation.