See all results for ''

Everyone knows interest rates have risen substantially over the last 12m but markets are still working through all the implications of a higher cost of capital. The three major risks to equity investors are derating, downgrades and debt refinancing, and as we go through this transition period they will take turns in being uppermost on people’s worry lists.

The crisis in mid-sized US banks over the last month serves as a reminder that investors need to be very wary of assets purchased or built with, or business models reliant on, an unsustainably low cost of capital. Ultimately, First Republic’s problem was that their cost of funding, which had already been rising as deposits repriced upwards, skyrocketed when they needed to replace lost deposits at 2% with wholesale funding at 5%.

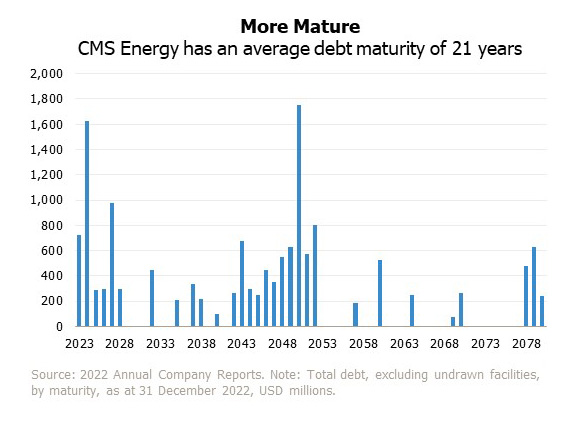

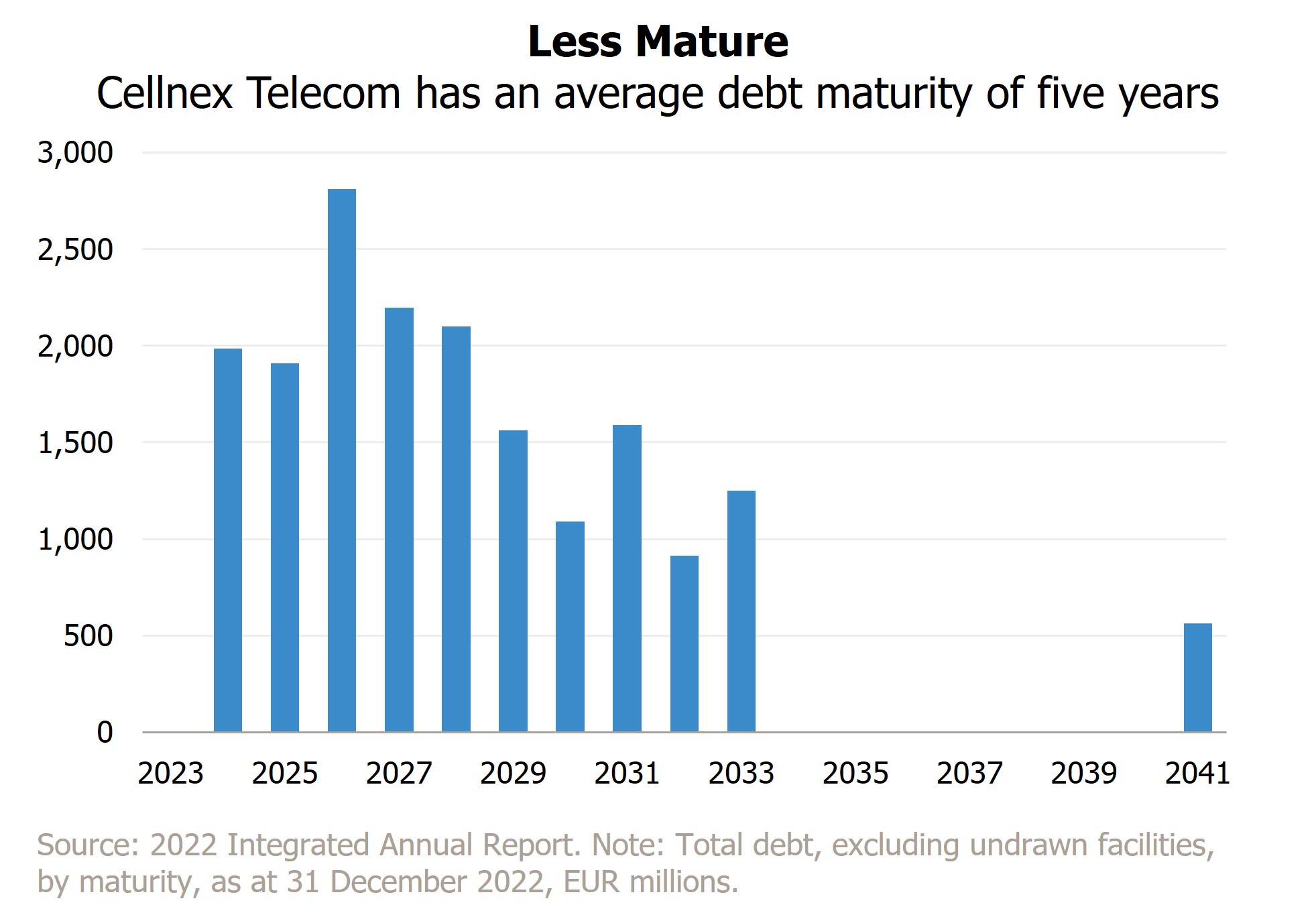

One obvious response is to run back to the safety of tech stocks with net cash on their balance sheets. The recent rotation in that direction is understandable, although we would caution that derating risk is not dead, just sleeping. It is equally easy to argue that in this environment you should just sell any company where financial gearing is an inherent part of the business model, for example financials or infrastructure. We disagree, but emphasise the importance of being selective. Not all infrastructure is funded in the same way. For example compare these two infrastructure-based companies, CMS Energy, a US regulated utility which we own, with Cellnex, a European telecom tower company, which we don’t.

Both of these companies are expected to face rising interest costs in the coming years but for CMS it is likely to be a much more manageable trajectory than for Cellnex.

We would also make two broader points:

All data Bloomberg or J O Hambro unless otherwise stated.

Disclaimer

This is a marketing communication.

Information on the rights of investors can be found here.

The registrations of the funds described in this communication may be terminated by JOHCM at its discretion from time to time. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile.

As the cost of capital has risen, so has volatility. What’s causing it ... and how should investors respond?

For a better experience, we recommend viewing this website in landscape orientation.